The Great Pivot — How Eight Months Rewrote the Rules (2025–2026)

From a three-day policy blitz to the first Commission-level crypto framework — the story of how enforcement-first became framework-first.

The previous post in this series — The Warning Years — ended with a question hanging in the air. By December 2024, every intellectual ingredient for a comprehensive crypto framework already existed: the DAO Report's substance-over-form principle, Hinman's flawed but prophetic intuition about dynamic securities status, Torres's separation of asset from transaction, and seven years of proof that open-ended factor tests don't work.

What was missing wasn't the ideas. It was the institutional will to assemble them.

On January 20, 2025, that will arrived — all at once.

Chapter 3: The Three-Day Revolution (January 2025)

Day One: The Executive Order

On January 20, 2025 — inauguration day — the White House published Executive Order 14178, titled "Strengthening American Leadership in Digital Financial Technology." The order established a Presidential Working Group on Digital Asset Markets and declared it the policy of the United States to support "the responsible development of digital assets."

Three days later, on January 23, the SEC issued Staff Accounting Bulletin No. 122, officially withdrawing SAB 121 — the Gensler-era rule that had required banks to recognize a dollar-for-dollar liability on their balance sheets for any crypto assets held in custody. SAB 121 had effectively made crypto custody uneconomical for traditional financial institutions. Its removal was retroactive, applying to fiscal periods beginning December 15, 2024.

In three days, the regulatory posture of the United States toward crypto shifted from containment to competition.

The Task Force

Between the executive order and the SAB, on January 21, Acting Chairman Mark Uyeda had established the SEC's Crypto Task Force, replacing Gensler's "Crypto Assets and Cyber Unit." The Unit had been an enforcement weapon. The Task Force was designed as a policy instrument.

Uyeda appointed Commissioner Hester Peirce to lead it. The symbolism was unmistakable. Peirce had spent five years as the SEC's most visible internal critic — the Commissioner who dissented against NFT enforcement, proposed a Token Safe Harbor the Commission never adopted, and publicly declared that the SEC "has not created an environment within which good activity can flourish." Now she was being asked to build that environment.

The Task Force's mandate was broad: engage with industry, develop clear regulatory guidelines, and — critically — resolve "what the SEC has done wrong in the past." After nine years of enforcement without rules, the agency was being asked to write the rules.

Chapter 4: The Controlled Demolition (February–August 2025)

What followed over the next eight months was not gradual reform. It was a systematic dismantling of the enforcement-first regime — conducted through three parallel channels.

Channel 1: The Staff Statement Cascade

Between February and August 2025, the SEC's Division of Corporation Finance issued a series of Staff Statements, each one declaring a category of crypto assets to be outside the scope of federal securities laws.

February 27 — Meme Coins. The first statement declared that meme coins — tokens with no underlying project, no roadmap, no promise of utility — are not securities. The reasoning: buyers of meme coins are "speculating on the success of their own promotional efforts or the collective hype of the community," not relying on the essential managerial efforts of an identifiable third party. The fourth prong of Howey fails.

March 20 — Proof-of-Work Mining. Mining activities on proof-of-work blockchains constitute "administrative or ministerial activity," not the kind of "essential managerial efforts" that create an investment contract. Miners are performing a service, not investing in a common enterprise.

April 4 — Covered Stablecoins. USD-backed stablecoins with a fixed one-to-one redemption mechanism are not securities. They are marketed and used as payment instruments, not as investments. No reasonable buyer purchases USDC expecting to earn a profit.

Later in the year, additional statements addressed broker-dealer custody requirements (May), leveraged and margin spot trading in a joint statement with the CFTC (September), and an expanded broker-dealer custody framework including Customer Protection Rule and Net Capital Rule guidance (December).

Each statement was narrow, carefully scoped, and technically staff-level rather than Commission-level. But taken together, the cascade drew a map. One by one, the SEC was identifying the categories of crypto activity that did not require securities registration — building a framework not by defining what was inside, but by marking what was outside.

For anyone paying close attention, the five-category architecture of Release 33-11412 was already visible in outline.

Channel 2: The Lawsuits Dissolve

While the Staff Statements rebuilt the conceptual framework, the SEC was simultaneously unwinding its enforcement legacy.

February 27 — Coinbase. The SEC and Coinbase filed a joint motion to dismiss the case with prejudice. The stated reason: to allow the Crypto Task Force to "develop the regulatory framework for crypto assets." The case that had symbolized the Catch-22 — the SEC suing a company for failing to comply with rules the SEC refused to write — was over.

May 29 — Binance. Joint motion for dismissal with prejudice. No re-litigation permitted. The most comprehensive crypto enforcement action ever filed quietly closed.

August — Ripple. On August 7, the SEC and Ripple reached a settlement; the court approved it on August 22. Both sides withdrew their appeals. The original $125 million penalty was reduced to $50 million. The case that had produced Judge Torres's landmark split decision — the ruling that separated the asset from the transaction — ended not with a Supreme Court precedent but with a negotiated close. The principle survived; the litigation did not.

Between February and August, the three defining lawsuits of the Gensler era all ended — not through adjudication, but through strategic withdrawal. The message was clear: the new SEC considered the old SEC's enforcement campaign a policy it inherited, not a principle it endorsed.

Channel 3: Congress Moves

The third channel was legislative. For the first time, Congress successfully passed federal crypto legislation.

The GENIUS Act (July 2025). The "Guiding and Establishing National Innovation for U.S. Stablecoins Act" passed both chambers with bipartisan majorities and was signed into law on July 18, 2025. It was the first federal law specifically regulating a category of crypto assets. The Act established a licensing framework for stablecoin issuers, required full reserves and regular audits, and — critically — explicitly excluded "payment stablecoins" from the definition of securities. The SEC's April 4 Staff Statement had already reached the same conclusion; Congress now codified it.

The CLARITY Act (July 2025). The "Digital Asset Market Clarity Act" — formally H.R. 3633 — passed the House 294–134 on July 17. Where FIT21 had died in the Senate a year earlier, the CLARITY Act was its successor — refined and strengthened.

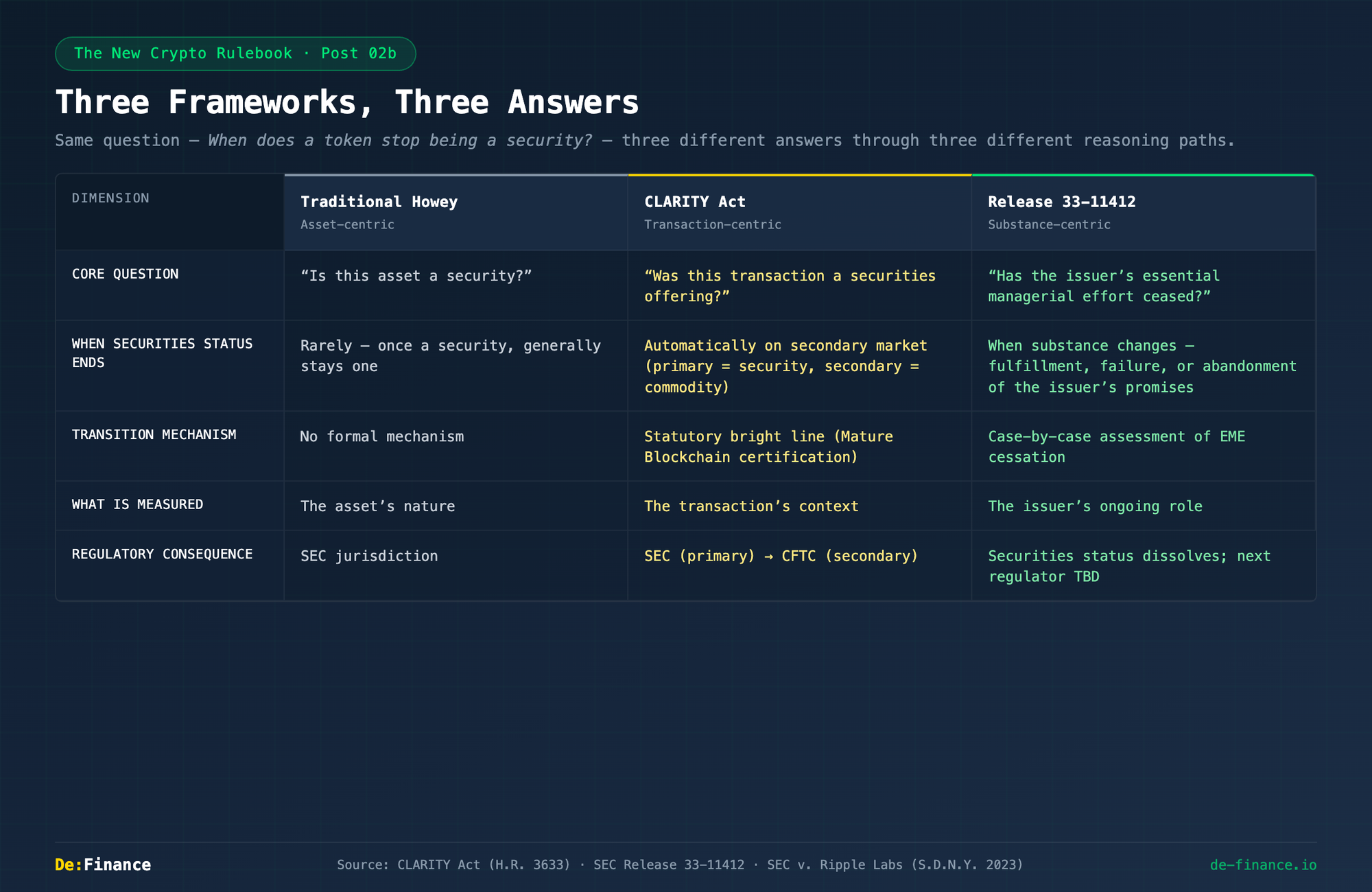

The Act's ambition was structural: to draw a statutory bright line between SEC and CFTC jurisdiction over crypto assets. Its five Titles carved up the regulatory landscape. Title I defined the key terms — "digital commodity," "investment contract asset," "restricted digital asset" — and mandated joint SEC-CFTC rulemaking. Title II governed primary offerings: tokens sold as part of an investment contract would be securities at the point of sale, but could transition to commodity status once the underlying blockchain met a statutory "maturity" threshold. Titles III and IV created parallel registration regimes — for SEC-regulated intermediaries handling digital securities (Title III) and for new CFTC-regulated categories: Digital Commodity Exchanges, Brokers, and Dealers (Title IV). Title V mandated studies on DeFi, NFTs, and financial literacy.

Three innovations stood out. First, the crude "20% Rule" from FIT21 for determining decentralization was replaced by a four-prong "Mature Blockchain System" test — requiring functional use, open-source code, no single entity controlling 20% or more of supply, and no de facto control over the network. An issuer could file a Certification of Maturity with the SEC; if the Commission took no action within 60 days, the blockchain was automatically deemed mature and its native token migrated from SEC to CFTC jurisdiction.

Second, FIT21's notice-of-intent registration model was upgraded to a Provisional Registration Regime: exchanges and brokers could operate for up to 270 days under provisional status while achieving full compliance, creating a regulatory on-ramp that imposed obligations without demanding full registration on day one. New issuers raising under $75 million in a twelve-month period could qualify for an exemption from full registration — though they still faced heightened disclosure requirements covering source code, governance, tokenomics, and use of proceeds.

Third, the Act adopted a transaction-centric reading of the Howey test rather than an asset-centric one. The same token could be a security when sold by the issuer (primary offering) and not a security when resold on the secondary market — a statutory codification of the logic Judge Torres had applied in the Ripple programmatic-sales ruling.

It's worth pausing here to note how the CLARITY Act's approach relates to — but differs from — the Separation doctrine that Release 33-11412 would later introduce. Both frameworks address the same practical question: when does a token stop being a security? But they arrive at different answers through different reasoning:

The CLARITY Act creates a jurisdictional answer (who regulates), while Release 33-11412's Separation creates a substantive answer (what the asset is). As the CLARITY Act moves through the Senate, one of the unresolved tensions is how these two mechanisms will interact — particularly for assets that might qualify as "mature" under the Act's structural test but still depend on essential managerial efforts under the Release's substance test.

The CLARITY Act also explicitly excluded meme coins and NFTs from both SEC and CFTC jurisdiction — creating a "neither securities nor commodities" category that drew sharp criticism from consumer advocates who warned of investor protection gaps in an asset class where retail loss rates exceed 90%.

As of early 2026, the CLARITY Act was still working through the Senate, where the Agriculture Committee had passed a companion bill (S. 3755) in January 2026 but the Banking Committee had stalled over a stablecoin yield dispute with the GENIUS Act framework. But the Act's DNA — the classification architecture, the maturity test, the transaction-centric Howey reading, the dual-regulator framework — had already been transmitted to the SEC.

Chapter 5: The Roundtable Sprint (March–December 2025)

Between the policy announcements and the legislative action, the Crypto Task Force ran a parallel process that would prove equally consequential: six public roundtables between March and December 2025, each one tackling a specific dimension of crypto regulation.

The roundtables served a dual purpose. Publicly, they were consultations — opportunities for industry, academics, and regulators to build consensus. Privately, they were the SEC's homework assignments: each roundtable mapped directly to a section of the framework that would eventually become Release 33-11412.

Roundtable 1 (March 21) — "How We Got Here and How We Get Out: Defining Security Status." The inaugural session reached a broad consensus that the existing SEC registration pathways were inadequate for crypto, and that the industry needed ex-ante rules rather than ex-post enforcement. This roundtable planted the seeds for the Release's five-category taxonomy.

Roundtable 4 (May 12) — "Tokenization: Moving Assets Onchain." The key framing that emerged: tokenization is not a new asset class but an evolution of market infrastructure. Chairman Paul Atkins — who had taken office in April — declared issuance, custody, and trading as his three priority areas. The distinction between "native issuance" and "tokenized representation" that surfaced here would become the Release's dividing line between digital securities and other categories.

Roundtable 5 (June 9) — "DeFi and the American Spirit." Atkins praised the Division of Corporation Finance's staff statements and then made a pointed observation: those statements were still "staff-level views," not "duly promulgated rules." The SEC needed to upgrade its guidance to Commission-level authority. This was, in effect, a public announcement of the Release's future status — not staff guidance, but a formal interpretive rule.

The remaining roundtables — on trading regulation, custody, and financial surveillance — addressed infrastructure questions that would be deferred to the subsequent Regulation Crypto Assets rulemaking. But the first five roundtables had already done their work. By December 2025, the intellectual architecture of the Release had been publicly debated, stress-tested, and refined through six months of open consultation.

The enforcement-first SEC had built its framework through litigation, in courtrooms where only the parties had standing. The framework-first SEC built its architecture in public, with transcripts.

Chapter 6: The Framework Arrives (2026)

Project Crypto

On January 29, 2026, Chairman Atkins and CFTC Chair Michael Selig stood together to announce "Project Crypto" — a formal joint initiative to coordinate digital asset regulation between the two agencies. The initiative had six focus areas: joint interpretation and rulemaking, clearing and margin frameworks, dual-registered exchange pathways, fit-for-purpose regulation, reporting simplification, and cross-market enforcement coordination.

The announcement was significant not for what it promised — the details were still to come — but for what it represented. After years of jurisdictional turf wars (the SEC claiming crypto was securities, the CFTC claiming it was commodities, neither agency willing to concede ground), the two regulators were publicly committing to a shared framework. The bureaucratic cold war was over.

In March, the agencies formalized this commitment through a Memorandum of Understanding establishing coordination mechanisms for overlapping jurisdictions.

Release 33-11412

On March 17, 2026, the SEC published Release No. 33-11412 / 34-105020. The full title was bureaucratic. The effect was not.

For the first time in the nine years since the DAO Report, the SEC issued a Commission-level — not staff-level — interpretive framework for crypto assets. It classified digital assets into five categories (digital commodities, digital collectibles, digital tools, covered stablecoins, and crypto asset securities), established the Separation doctrine (the mechanism by which a token's securities status can dissolve when the issuer's essential managerial efforts cease), and replaced the 2019 Framework's open-ended factor test with a structural classification system.

The Release was published as an interpretive rule, taking effect on March 23 — six days after publication. Under the Administrative Procedure Act, interpretive rules are exempt from notice-and-comment requirements. The SEC was able to move fast precisely because the Release interpreted existing law rather than creating new rules.

But Chairman Atkins was careful to describe the Release as "a beginning, not the end." The binding rules — the detailed registration requirements, trading regulations, and compliance obligations — would come through a separate notice-and-comment rulemaking: Regulation Crypto Assets, expected in the summer of 2026. The Release drew the map. Regulation Crypto Assets would pave the roads.

Epilogue: The Harvest

Look at the speed of what happened. In roughly fourteen months — from the January 2025 executive order to the March 2026 Release — the SEC went from enforcement-first to framework-first, systematically classified crypto assets, wound down the major lawsuits, and published the most comprehensive regulatory interpretation the industry had ever seen.

How was this possible? How do you build in fourteen months what couldn't be built in nine years?

The answer is that it wasn't built in fourteen months. It was harvested.

Every major element of Release 33-11412 has a direct ancestor in the wreckage of 2017–2024:

The five-category taxonomy descends from the DAO Report's principle that economic substance, not technological form, determines regulatory treatment. The same principle, applied systematically, produces named categories with defined boundaries — replacing the 2019 Framework's "weigh all the circumstances" with "if it fits this category, here's the answer."

The Separation doctrine is the direct descendant of Hinman's "sufficiently decentralized" — stripped of its legal deficiencies, grounded in Howey's fourth prong, and formalized as a Commission-level mechanism rather than a personal speech. The intuition survived. The improvisation did not.

The asset-is-not-the-security principle was stated most clearly by Judge Torres in the Ripple decision: the same XRP token produced opposite legal conclusions depending on the context of the sale. The Release elevated this distinction from a district court ruling to a governing framework principle.

And the structural classification approach itself — replacing open-ended factor lists with named categories — was the lesson the 2019 Framework taught by failing. Seven years of "it depends on the circumstances" proved, by exhaustion, that circumstantial tests cannot scale.

The enforcement-first era didn't produce a framework. But it produced every idea the framework needed. The paradigm shift of 2025 didn't invent new concepts — it assembled existing ones, under political conditions that finally made assembly possible.

This is the paradox at the heart of Release 33-11412. The document that marks the end of enforcement-first is itself a product of enforcement-first. The nine years of regulatory chaos weren't wasted. They were — inadvertently, expensively, and often unjustly — the research phase.

The framework arrived not despite the chaos, but because of it.

This is Part 2b of "The New Crypto Rulebook" series. For Part 2a — the enforcement era that built the raw materials — see The Warning Years. For the five-category framework itself, see Post 1c: Inside the Release. Next in the series: Post 3 — Securities Regulation Is Political.

Sources

Executive Actions & SEC Bulletins

- Executive Order 14178 — Strengthening American Leadership in Digital Financial Technology (White House, Jan. 20, 2025)

- Staff Accounting Bulletin No. 122 (SEC, Jan. 23, 2025) — withdrawal of SAB 121

Crypto Task Force

- SEC Crypto 2.0: Acting Chairman Uyeda Announces Formation of New Crypto Task Force (SEC Press Release 2025-30, Jan. 21, 2025)

- Crypto Task Force Homepage (SEC)

Staff Statements (Division of Corporation Finance)

- Staff Statement on Meme Coins (Feb. 27, 2025)

- Statement on Certain Proof-of-Work Mining Activities (Mar. 20, 2025)

- Statement on Stablecoins (Apr. 4, 2025)

Enforcement Dismissals

- SEC Announces Dismissal of Civil Enforcement Action Against Coinbase (SEC Press Release 2025-47, Feb. 27, 2025)

- Binance Holdings Limited et al. — Litigation Release (SEC LR-26316, May 29, 2025)

- Ripple Labs, Inc. — Litigation Release (SEC LR-26369, Aug. 2025)

Legislation

- GENIUS Act — Public Law 119-27 (signed July 18, 2025)

- CLARITY Act — H.R. 3633 Full Text (119th Congress)

- CLARITY Act Section-by-Section Analysis (House Financial Services Committee)

- The Facts: The CLARITY Act (Senate Banking Committee)

Joint Regulatory Framework (2026)

- Opening Remarks at Joint SEC-CFTC Harmonization Event — Project Crypto (SEC, Jan. 29, 2026)

- SEC and CFTC Announce Historic Memorandum of Understanding (SEC Press Release 2026-26, Mar. 2026)

- SEC Clarifies the Application of Federal Securities Laws to Crypto Assets (SEC Press Release 2026-30, Mar. 17, 2026) — Release 33-11412 announcement

- Release No. 33-11412 — Full Document (PDF) (SEC, 68 pages)

- Release 33-11412 Fact Sheet (PDF) (SEC)

Critical Perspectives

- AFR Fact Sheet: The CLARITY Act — A Consumer Catastrophe (Americans for Financial Reform)

- Consumer Reports Letter Opposing CLARITY Act