Before the Rulebook — The Howey Test and Why 'Efforts of Others' Is the Only Question That Matters

Before the five-category framework makes sense, you need the test it is built on — and the single prong that does all the heavy lifting.

1. What the Howey test actually asks

The U.S. Supreme Court decided SEC v. W.J. Howey Co. in 1946. The case involved Florida orange groves, but the four-part test it produced has governed every "is this a security?" question since — including the ones now being asked about crypto.

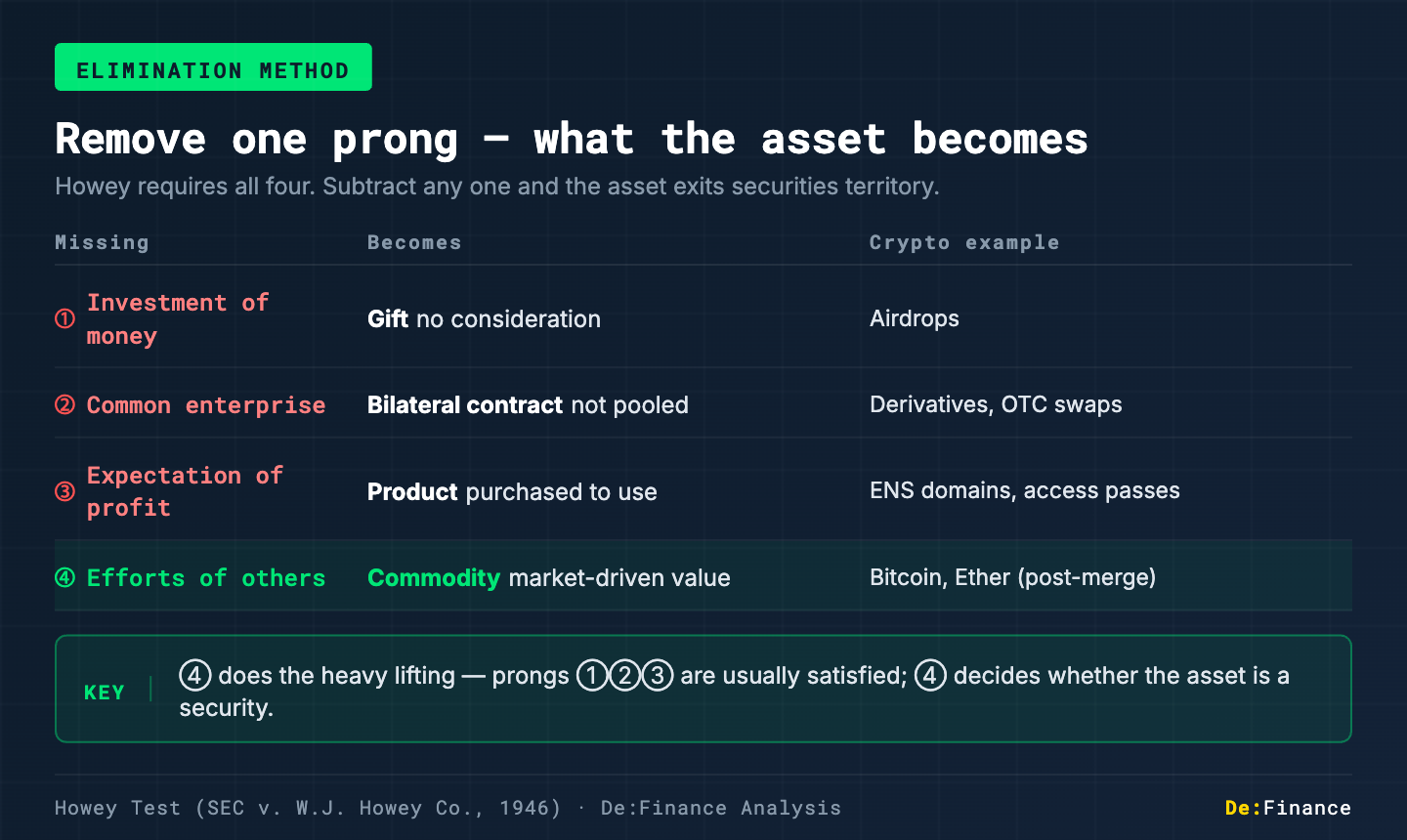

An asset is an investment contract (and therefore a security) if all four elements are present:

| # | Element | The question it asks |

|---|---|---|

| 1 | Investment of money | Did the buyer pay something of value? |

| 2 | Common enterprise | Are the buyers' fortunes pooled and tied to the success of a shared venture? |

| 3 | Expectation of profit | Did the buyer acquire this to earn a return, not to use it? |

| 4 | Efforts of others | Does the expected return depend primarily on someone else's managerial decisions? |

All four must be satisfied. Remove any single element and the asset is not an investment contract — it is something else entirely. What it becomes depends on which element is missing.

2. The elimination method: what happens when you subtract one prong

This is the move that makes the Howey test useful for crypto. Instead of asking "are all four present?", ask "which one is missing?" — because the missing element tells you exactly what the asset is.

Only when all four are present does the asset sit in the investment contract (= security) category, triggering the full regulatory apparatus: mandatory disclosure, insider-trading prohibition, and supervisory jurisdiction.

The logic is more than academic. Release 33-11412 maps each of its five categories to one of these elimination outcomes. The release did not invent this mapping, but it is the first Commission-level document to make it explicit.

3. Why "efforts of others" does all the heavy lifting

In practice, elements ① and ② are easy to satisfy for most token projects. Someone paid crypto or fiat (①), and the token's value is tied to a shared ecosystem (②). Element ③ — expectation of profit — is contested in edge cases (pure utility tokens, stablecoins), but for most tokens, the market reality is that holders expect appreciation.

That leaves element ④ — the efforts of others — as the decisive prong in the vast majority of crypto disputes. Every major SEC enforcement action of the last decade turned on this question: Is there an identifiable team whose discretionary managerial decisions drive this token's value?

To see why this is the question that matters, it helps to think about what securities regulation is actually for.

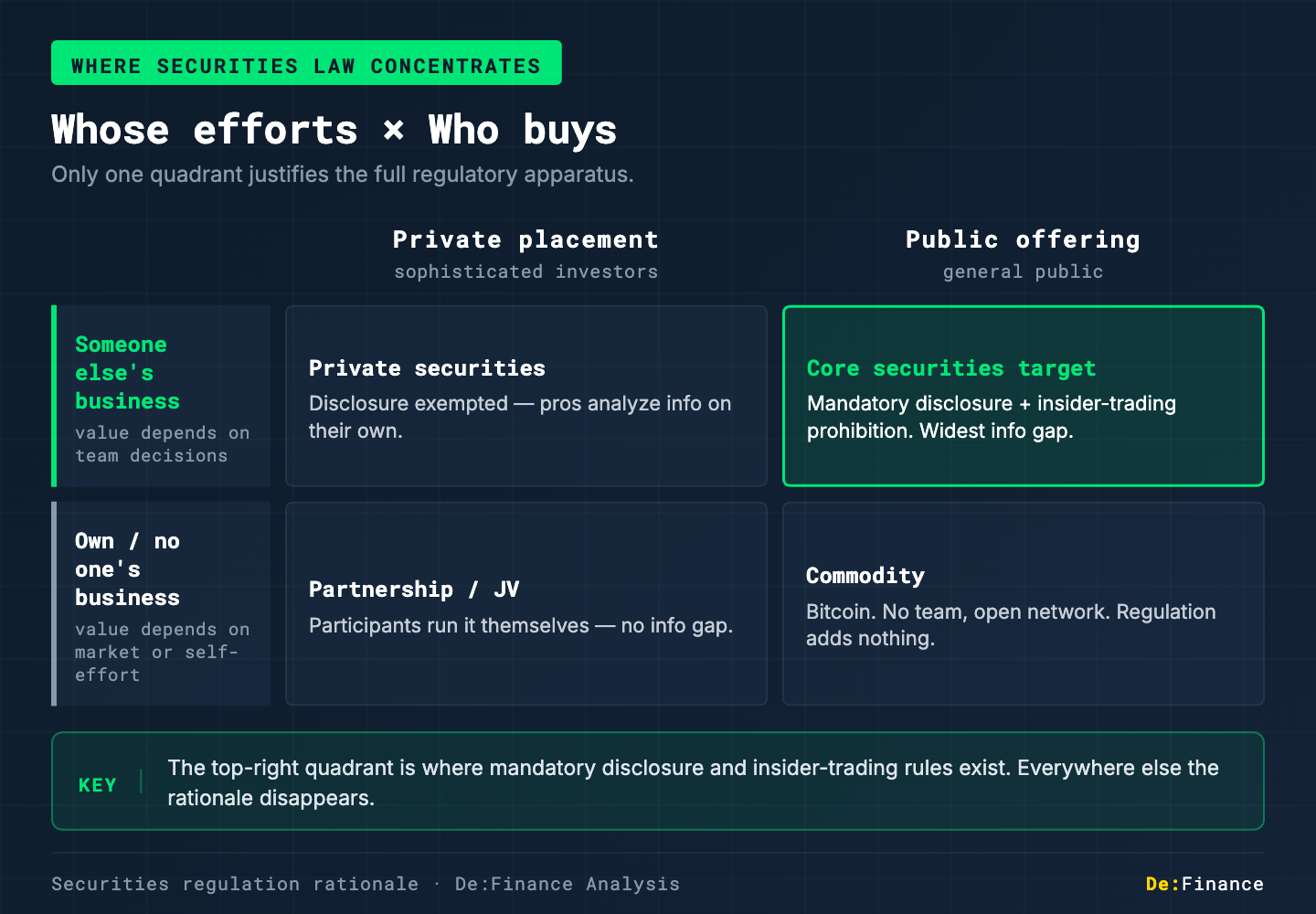

4. The real purpose of securities law: information asymmetry

Securities regulation exists because of one structural problem: information asymmetry. When you buy a physical good — a car, a bag of rice — you can inspect it. When you buy a security, you are buying an intangible claim whose value depends on information the issuer knows before you do: next quarter's revenue, a pending partnership, the CEO's plan to sell shares.

The entire apparatus of mandatory disclosure and insider-trading prohibition is built to close that gap. If no gap exists — if no insider has privileged information — there is nothing for securities law to regulate.

This produces a clean two-by-two frame:

The top-right quadrant is where securities law concentrates its force. The bottom-right is where Bitcoin sits — and where every token that successfully argues "we are sufficiently decentralized" wants to be.

This matrix is the conceptual engine behind Release 33-11412. The five-category framework is, at its core, a method for placing each crypto asset in one of these four quadrants. And the single variable that moves an asset from the top row to the bottom row — from "someone else's business" to "no one's business" — is the Howey test's fourth element: efforts of others.

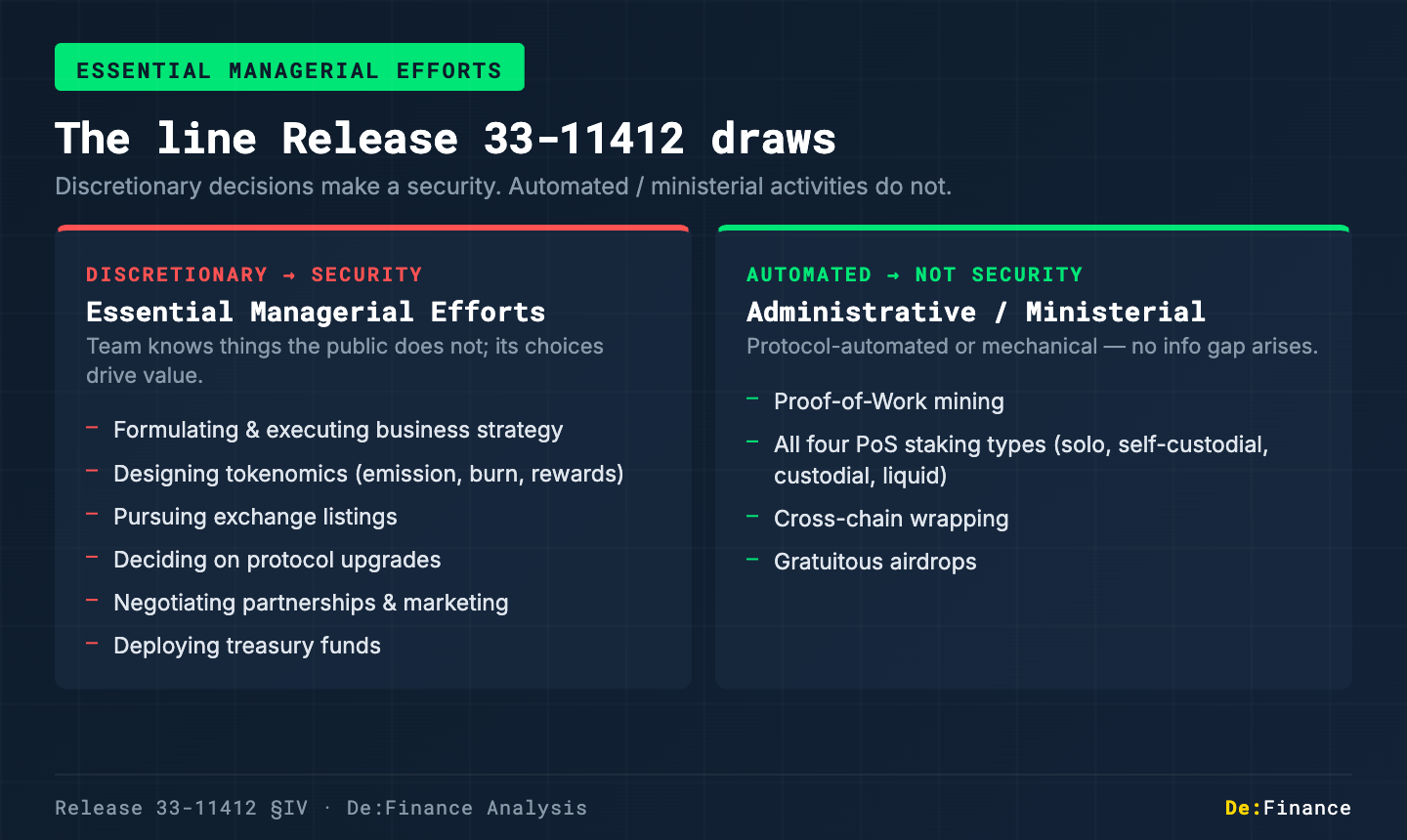

5. "Essential managerial efforts" — the line the release draws

The release sharpens the "efforts of others" prong into a specific operational test: essential managerial efforts versus administrative or ministerial activities.

Essential managerial efforts are discretionary decisions where the team knows the outcome before the market does. Insider information is structurally inevitable:

- Formulating and executing business strategy

- Designing or modifying tokenomics (emission rates, burn ratios, staking rewards)

- Pursuing exchange listings

- Deciding on protocol upgrades

- Negotiating partnerships and marketing campaigns

- Deploying treasury funds

Administrative or ministerial activities are either automated by protocol code or performed by the token holder herself. No team is making discretionary calls; no information gap arises:

- Proof-of-Work mining

- All four types of Proof-of-Stake staking (solo, self-custodial, custodial, liquid)

- Cross-chain wrapping

- Gratuitous airdrops

The distinction is intuitive once you see it through the information-asymmetry lens. Mining rewards are computed by an algorithm anyone can read. Staking yields are set by protocol parameters visible on-chain. But when a team decides to change the burn rate from 96% to 50%, or to redirect emissions from one chain to another, or to pursue a listing on a major exchange — those decisions happen behind closed doors, and the market learns about them after the fact. That is the gap securities law is built to close.

6. What the release chose to focus on — and what comes next

Release 33-11412 is built entirely around this essential-managerial-efforts line. Every classification it makes — which tokens are commodities, which are collectibles, which are tools, which are securities — is an answer to the same question: Does a team's discretionary decision-making drive this asset's value?

That focus is deliberate. Of the four Howey prongs, "efforts of others" was the one that generated the most litigation, the most uncertainty, and the most industry frustration over the past decade. By drawing a bright line through it — and by explicitly stating that mining, staking, wrapping, and airdrops fall on the non-security side — the release resolves the largest cluster of open questions in a single document.

But it does more than classify. The release introduces a concept called separation — the idea that a token can start as part of an investment contract and later stop being one, as the project matures and the team's essential efforts become less essential. This is arguably the most consequential legal innovation in the document.

The next post walks through both: the five categories the release creates, and the separation concept that lets tokens move between them.