How SEC Release 33-11412 Lands in Korea

A 15-month arc, a new five-category framework, and what it means for anyone planning to build in, invest in, or launch a token into the Korean market.

1. The release that closed a chapter

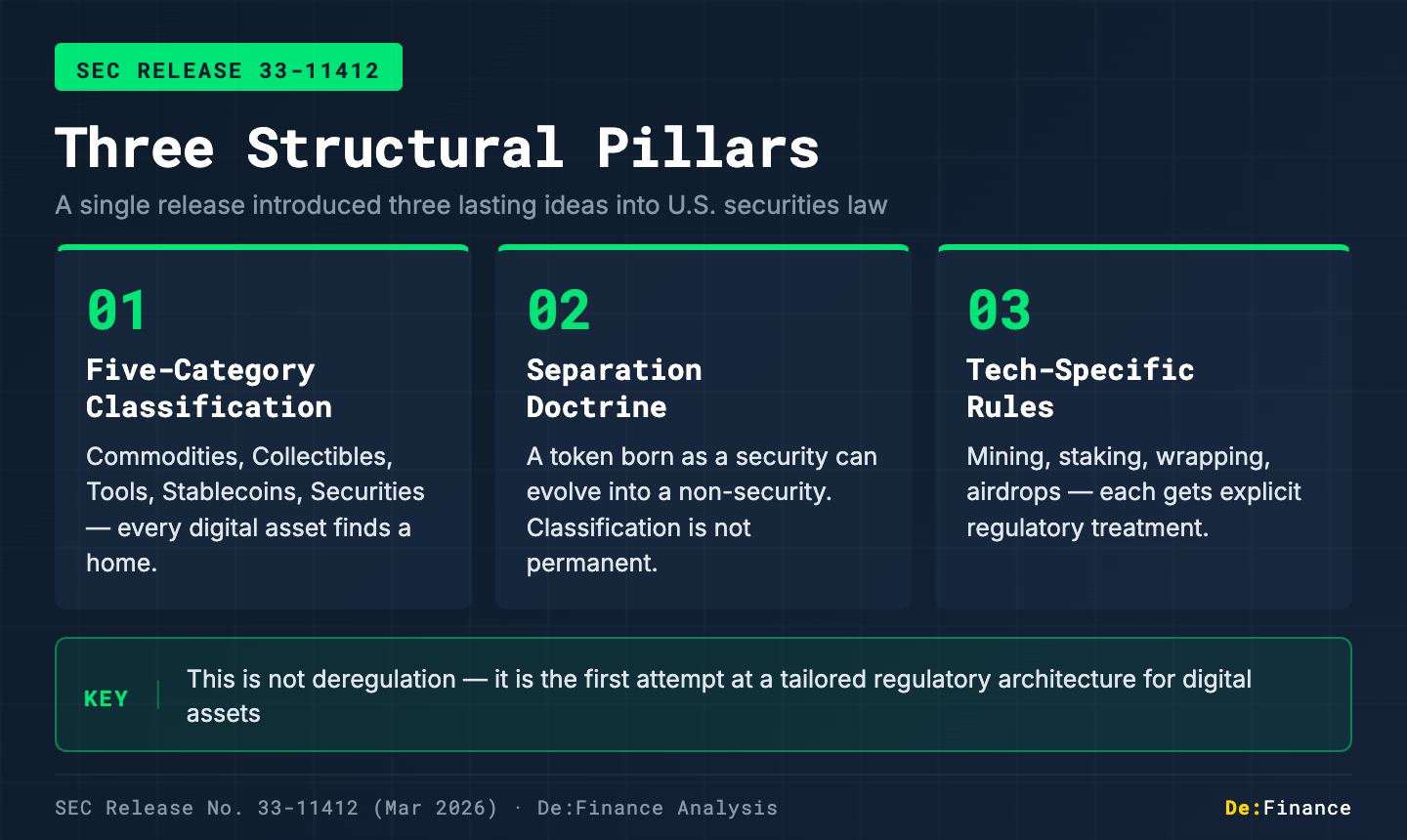

On March 17, 2026, the U.S. Securities and Exchange Commission and the Commodity Futures Trading Commission jointly issued Release No. 33-11412 / 34-105020, an interpretive rule that sorts crypto assets into five categories — digital commodities, digital collectibles, digital tools, stablecoins, and digital securities — and explains how the federal securities laws apply to each. The release also contains dedicated sections on wrapped tokens (§VI) and airdrops (§VII).

The release is less a surprise than a consolidation. Throughout 2025, the SEC's Division of Corporation Finance published a sequence of staff statements covering meme coins, proof-of-work mining, certain stablecoins, protocol staking, and liquid staking. Release 33-11412 pulls those staff-level views onto a common analytical frame and elevates them to the Commission itself. Because it is an interpretive rule, it is exempt from APA notice-and-comment and took effect immediately on March 23, 2026. In its own words, it "does not itself create any new legal obligations" — its purpose is to "reduce uncertainty by finally providing clarity."

The binding rulemaking track is a separate document. Regulation Crypto Assets, the framework Chair Atkins unveiled in his March 17, 2026 Digital Chamber speech, will address how to regulate what the release classified: a Startup Exemption (roughly four years, ~$5M cap, principles-based disclosure building on Commissioner Peirce's Token Safe Harbor), a broader Fundraising Exemption, an Investment Contract Safe Harbor codifying when essential managerial efforts are complete, and an Innovation Exemption. As of April 7, 2026, the proposal is under OIRA review at the White House, with Atkins saying it will be published "shortly." Release 33-11412 answers "what is a security"; Regulation Crypto Assets will answer "how to regulate it." The two should not be conflated.

That's the U.S.-facing summary. For anyone building toward, investing in, or launching a token into the Korean market, the more useful question is how this release lands in Seoul — and that is where this blog sits.

2. Why this is a Korean story too

Korea's capital markets statute defines the "investment contract" security — tuja gyeyak jeunggwon — as a direct import of the U.S. investment contract doctrine. The Korean definition (Financial Investment Services and Capital Markets Act, Article 4(6)) mirrors the four Howey prongs: a common enterprise, an investment of money, profits expected primarily from the efforts of others, and a contractual right to those profits. The wording differs in a few meaningful places, but the scaffolding is unmistakably American.

Two consequences follow.

First, Korean regulators have relatively few domestic precedents to rely on. The Securities and Futures Commission's landmark recognition of a music royalty claim as an investment contract (the Musicow decision in April 2022) was its first headline case. Appellate courts have not yet ruled on whether any specific crypto asset qualifies as an investment contract security; the lower-court decisions that have addressed the question have said no. Wherever the statute is silent, practice reaches for U.S. case law and SEC interpretations as a supplementary reading frame.

Second, Korean enforcement has been strikingly asymmetric. In the traditional securities market, the Financial Services Commission (FSC) and Financial Supervisory Service (FSS) routinely pursue disclosure violations, insider trading, and unregistered offerings. In the tokenized-securities and fractional-investment space, regulators have been even more active: after Musicow, the FSC issued a fractional-investment guideline (April 2022) and the "Measures for Improving the Framework for Issuance and Distribution of Security Tokens" (February 2023), then forced restructuring on fractional-investment platforms operating in real estate, art, and agricultural assets. In the traditional and tokenized-securities lanes, the enforcement cycle runs end-to-end: interpret, determine, sanction.

The crypto-asset market is the exception. Korean regulators issued that February 2023 security-token guideline stating that any token meeting the investment-contract definition would be treated as a security under the Capital Markets Act, and they have repeated the message in various forms since. But no listed crypto asset has been suspended from trading because regulators determined it was an unregistered security. No Korean crypto exchange has been fined, formally cautioned, or sanctioned for distributing an unregistered security. The SFC has not named any specific crypto asset as an investment contract security in a public decision. The signal has been loud; the enforcement has been essentially absent.

That gap — active rhetoric, dormant enforcement — is why Korea tracks the United States on this question with unusual sensitivity. The Korean regulator has not committed to a hard line. It has, in effect, reserved the right to go either direction. And in a world where the SEC has just withdrawn roughly a dozen high-profile enforcement actions (Coinbase, Kraken, Binance, Ripple, Robinhood, and others) and issued a five-category taxonomy, there is very little interpretive room for Seoul to tighten where Washington has loosened.

None of this means the securities-law question has gone away for Korean crypto. It means the question is increasingly being answered by reference to what happens on the other side of the Pacific. Release 33-11412 is, in that sense, a Korean policy document by proxy.

3. What the U.S. has actually been building

Strip away the politics and the enforcement headlines, and the U.S. arc of the last 15 months is coherent on a single point: reducing Howey-test uncertainty and giving the industry a framework it can build against.

Three moves do most of the work.

Categorical clarity. Release 33-11412 places each crypto asset in one of five buckets and asks whether securities law applies only after that sorting. A meme coin is a digital collectible; a network-native utility token is a digital tool; a reserve-backed stablecoin is a stablecoin; a tokenized note on a real-world asset is a digital security. The Howey inquiry still exists, but it is no longer the opening filter. That shift alone eliminates a category of disputes that consumed years of litigation.

A lifecycle view of "efforts of others." The release draws a line between essential managerial efforts — the kind that make investors economically dependent on a promoter — and administrative or ministerial efforts that do not. A token launched by a small team of developers in a pre-network phase can plausibly sit on the "essential" side of the line; the same token, two years later, running on a decentralized network with thousands of independent participants, plausibly does not. "Once a security, always a security" is no longer the operating assumption. This is the biggest substantive change in the U.S. framework, and it is the one most likely to travel to Korea, because the Korean statute already uses the softer "primarily" (juro) formulation instead of Howey's original "solely."

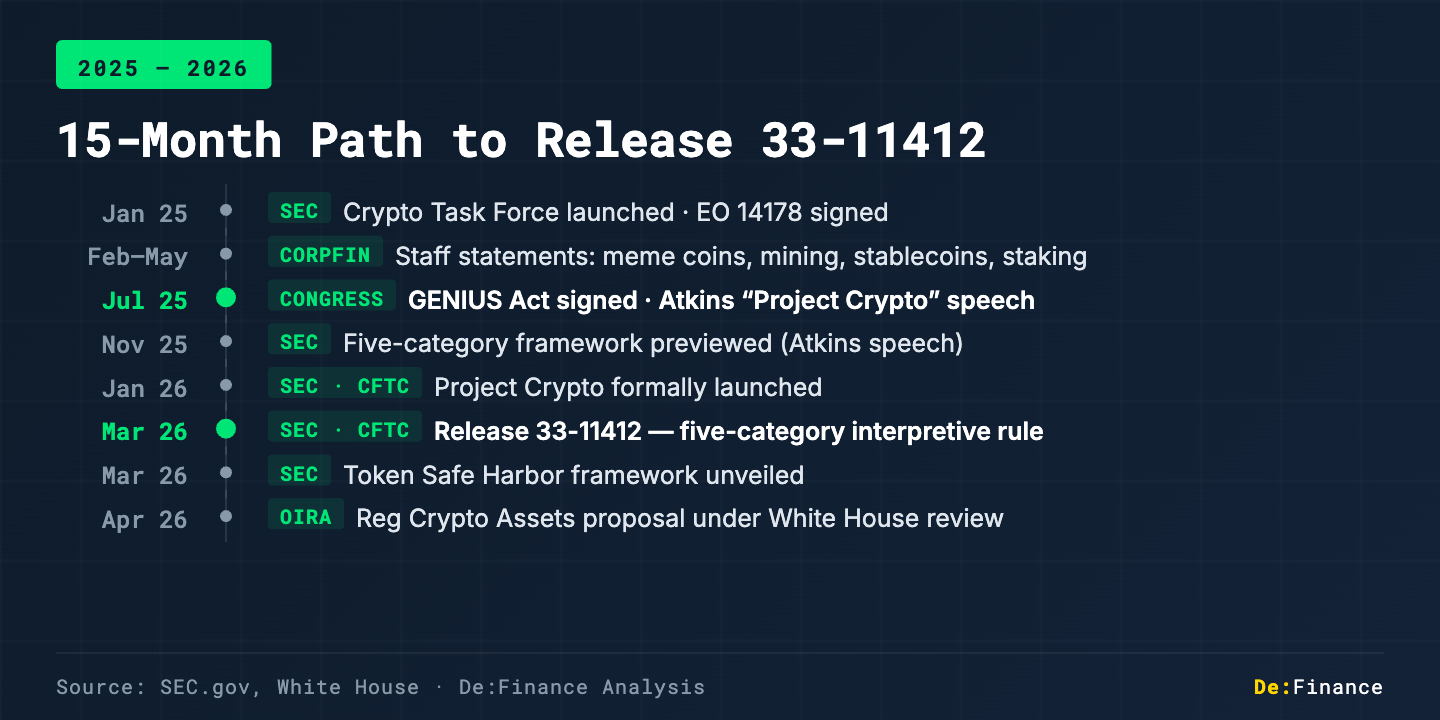

Enforcement retreat, rulemaking advance. Through 2025, the SEC closed or dismissed more than ten crypto enforcement actions that had been inherited from the prior administration. At the same time, Chair Paul Atkins used two "Project Crypto" speeches (July and November 2025) to say, in so many words, that the agency's approach would shift from enforcement-first to rulemaking-first. The five-category release is the first major delivery on that promise.

It is tempting to read these three moves as a simple deregulation story. That reading is incomplete. The real goal — stated explicitly in Executive Order 14178 (January 2025), the President's Working Group on Digital Asset Markets report (July 2025), and the GENIUS Act (stablecoins, signed in July 2025) — is industrial policy: the United States wants to be the venue where crypto infrastructure is built, regulated, and owned. Securities-law clarification is one lane of that project. When the SEC says the goal is to "provide clear rules of the road," it means something narrower and more specific than "deregulate": it means giving operators enough predictability to make capital-allocation decisions.

Korean founders, exchanges, and institutional allocators should read the release in that frame. It is not a free pass. It is a set of rules that is easier to comply with than the old set of rules, delivered by a regulator that wants the U.S. to host the activity.

4. A 15-month timeline (month resolution)

The following table lists only the events in the 2025-2026 arc that bear directly on securities-law treatment of crypto assets. Exchange-traded product approvals, custody rule changes unrelated to securities classification, and state-level developments are out of scope here and will appear in later posts.

| Date | Actor | Document or Event | Character |

|---|---|---|---|

| 2025-01 | SEC | Crypto Task Force established, led by Commissioner Hester Peirce | Formal signal of securities-classification review |

| 2025-01 | White House | Executive Order 14178, Strengthening American Leadership in Digital Financial Technology | Policy-direction reset |

| 2025-01 | SEC | Rescission of SAB 121; replacement with SAB 122 | Removes custody accounting barrier |

| 2025-02 | SEC (Division of Corporation Finance) | Staff Statement on Meme Coins | Meme coins generally not securities |

| 2025-03 | SEC (Division of Corporation Finance) | Staff Statement on Proof-of-Work Mining | Mining activities generally not securities |

| 2025-04 | SEC (Division of Corporation Finance) | Staff Statement on Certain Stablecoins | Reserve-backed stablecoins generally not securities |

| 2025-05 | SEC (Division of Corporation Finance) | Staff Statement on Protocol Staking Activities | Protocol staking generally not securities |

| 2025-07 | Congress / White House | GENIUS Act signed into law | Stablecoin statutory framework, non-security classification |

| 2025-07 | White House | President's Working Group on Digital Asset Markets report | Comprehensive policy roadmap |

| 2025-07 | SEC | Chair Atkins, "Project Crypto" speech | Formal shift from enforcement-first to rulemaking-first |

| 2025-08 | SEC (Division of Corporation Finance) | Staff Statement on Liquid Staking | Liquid staking generally not securities |

| 2025-11 | SEC | Chair Atkins, "Project Crypto: One Year In" speech | Five-category framework previewed |

| 2026-01 | SEC / CFTC | Project Crypto formally launched | Joint SEC-CFTC initiative |

| 2026-03 | SEC / CFTC | SEC-CFTC MOU | Formal jurisdictional coordination |

| 2026-03 | SEC / CFTC | Release No. 33-11412 / 34-105020, joint five-category interpretive rule | Commission-level consolidation; includes §VI Wrapping and §VII Airdrops; immediately effective |

| 2026-03 | SEC | Atkins speech, "Regulation Crypto Assets: A Token Safe Harbor" | Follow-up rulemaking framework unveiled |

| 2026-04 | SEC / OIRA | Regulation Crypto Assets proposal under OIRA review | Startup / Fundraising / Innovation Exemption + Investment Contract Safe Harbor; Federal Register publication imminent |

5. The thesis, in one line

The U.S. has moved to reduce classification uncertainty for crypto, and Korea's crypto market — because of how its statute was written and how its regulator has behaved for the past three years — has structural reasons to follow, not to resist.

Reading Release 33-11412 carefully is therefore no longer a U.S. exercise. The next post in this series walks through the release itself: the five categories, the essential efforts line, the lifecycle concept, the lifecycle concept, and how each 2025 staff statement sits inside the Commission-level framework.