Securities Regulation Is Political — Always Has Been, Always Will Be

Series: The New Crypto Rulebook — Decoding SEC Release 33-11412 Post role: WHY — Why this regulatory shift, and why it will not be the last Target: ~3,000 words Audience: Industry participants, investors, and policymakers who need to assess regulatory risk over time

Prologue — The Framework Arrived, But Politics Did Not Leave

The final sentence of Part 2b read:

"The framework did not arrive despite the chaos; it arrived because of the chaos."

That sentence captures one truth. It also obscures another.

The obscured truth is this — the framework arrived, but the politics did not leave.

On March 17, 2026, the SEC issued Release 33-11412. Six days later, it took effect. A five-category taxonomy, a separation doctrine, sixteen tokens explicitly classified as Digital Commodities — the clarity that had been absent for nine years finally arrived. Markets cheered. The industry, exhausted from the enforcement era, exhaled.

But step back, and a question lingers: Is this a permanent resolution?

The answer is straightforward. No. Release 33-11412 is not the end. It is the product of one political phase. And political phases end.

This article defends a simple thesis: securities regulation is, at its core, political. It was political in 1933, and it remains political today. The market-friendly tone of Release 33-11412 is not legal progress — it is one side of a long-running political pendulum.

Understanding that pendulum is not a matter of historical curiosity. It is a practical tool for anyone who must price regulatory risk over time — issuers, investors, exchange operators, and policymakers in jurisdictions (like Korea) that look to the United States as a regulatory reference point.

1. 1933 — Securities Law Was Born of Political Crisis

To understand where we are, we must return to where it began. Everything about modern American securities law — the Securities Act, the Exchange Act, the SEC itself, and ultimately the Howey test — flows from a single political crisis.

The Great Crash

October 1929 saw a cascade of crashes. On Thursday the 24th ("Black Thursday"), the Dow fell roughly 11%. On Monday the 28th ("Black Monday"), it fell about 13%. On Tuesday the 29th ("Black Tuesday"), another 12%. In six days, the index was effectively shattered. By July 8, 1932, the Dow had fallen from its September 3, 1929 peak of 381.17 to 41.22 — a loss of nearly 89%. Over the same period, US GDP contracted by roughly 30%, and unemployment reached about 25% in 1933.

But economic statistics alone did not drive policy. What drove policy was anger.

The Pecora Hearings (1932–1934)

On April 11, 1932, the US Senate Committee on Banking and Currency began hearings to investigate the causes of the 1929 crash. The real engine of those hearings was Ferdinand Pecora — a first-generation Sicilian immigrant lawyer appointed as Chief Counsel in January 1933.

Pecora opened up the internals of American finance to ordinary citizens for the first time. The facts he extracted:

- National City Bank (today's Citigroup) sold near-default Peruvian government bonds to retail investors; its president Charles Mitchell had also received $2.4 million in interest-free loans from the bank's own coffers.

- J.P. Morgan & Co. maintained a "preferred list" of friends-of-the-bank — among them former President Calvin Coolidge and Supreme Court Justice Owen J. Roberts — who were offered IPO shares at deeply discounted prices.

- Albert Wiggin, chairman of Chase National Bank, had shorted his own bank's stock during the crash, profiting roughly $4 million while the bank he led collapsed.

The hearings ran approximately two years (April 1932 to May 1934) and produced more than 12,000 pages of testimony. The public was furious.

1933–1934 — The Birth of the Law

For Franklin D. Roosevelt, who took office on March 4, 1933, the Pecora hearings provided political momentum. On May 27, 1933, Roosevelt signed the Securities Act of 1933 ("Truth in Securities Act"). Two pillars:

- Full disclosure — issuers must file a registration statement and provide a prospectus.

- Anti-fraud provisions — Section 17(a), criminal and civil liability for fraudulent issuance.

The following year, the Securities Exchange Act of 1934 regulated secondary markets, and the Securities and Exchange Commission (SEC) was established to enforce both Acts. Roosevelt's first SEC chairman was — in a remarkable irony — Joseph P. Kennedy, himself a Wall Street operator of the kind Pecora had been hunting.

The Insight

Securities law was not the product of organic market evolution. It was a political response to a political crisis.

Without the 1929 crash, without Pecora's revelations, without Roosevelt's 1932 election — modern American securities law as we know it would not exist, or would look very different.

This is not merely historical trivia. If the birth of the law was political, so is its application. The same statute is enforced strongly in some periods and weakly in others. That is the topic of the next chapter.

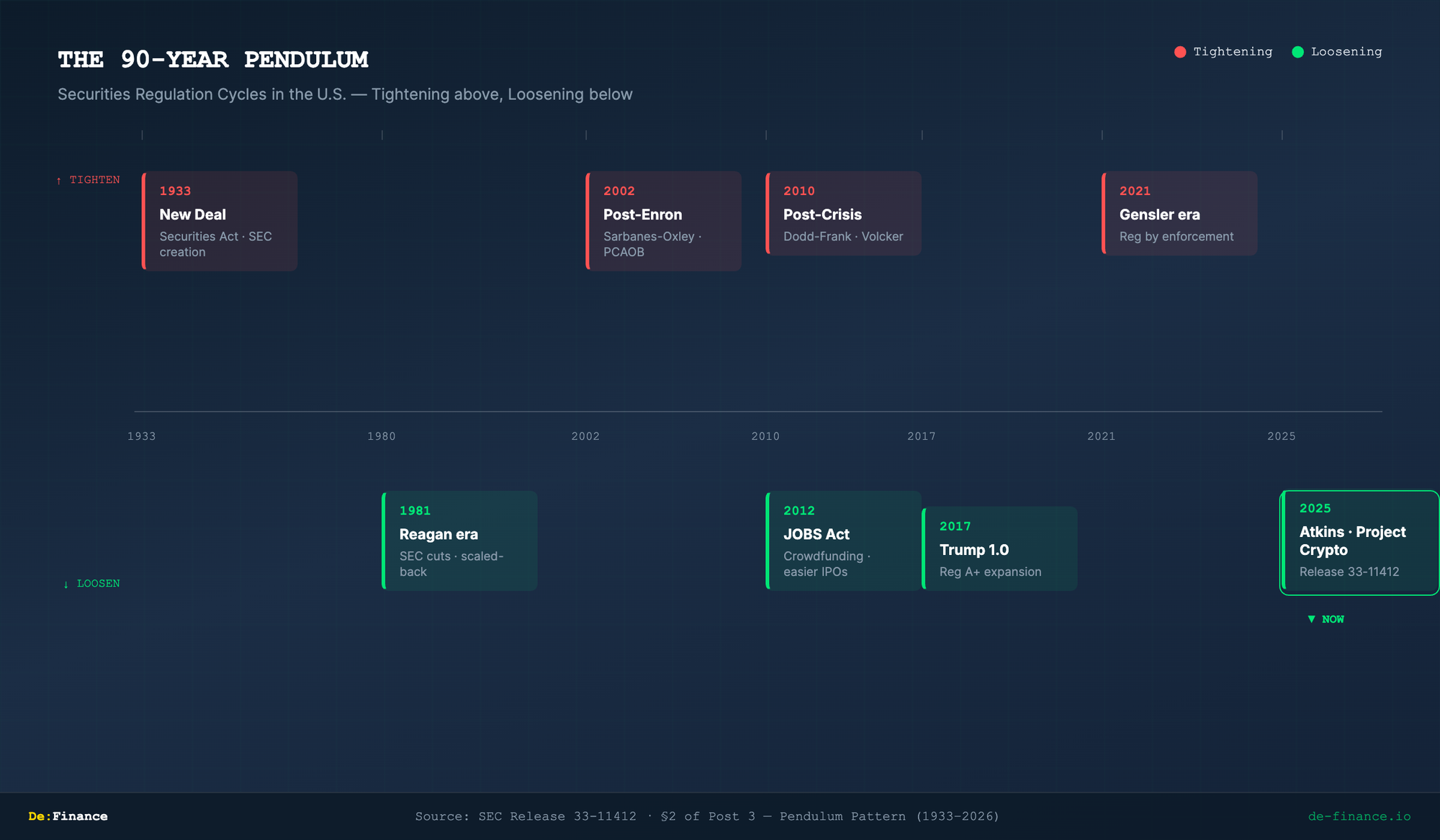

2. The Pendulum — A 90-Year Pattern

In the ninety years since 1933, the SEC has repeated one pattern: tightening → loosening → tightening → loosening.

Tightening Phases

Each tightening phase was triggered by a major market event or political crisis.

| Phase | Trigger | Key Action |

|---|---|---|

| New Deal (1933–) | 1929 Crash | Securities Act, Exchange Act, SEC creation |

| Post-Enron (2002–) | Enron / WorldCom accounting fraud (2001–2002) | Sarbanes-Oxley Act, PCAOB creation |

| Post-Financial Crisis (2010–) | 2008 Global Financial Crisis | Dodd-Frank Act, Volcker Rule |

| Gensler era (2021–2025) | DeFi excess, ICO residue, FTX collapse (2022) | Regulation by enforcement |

In each case: major market failure → political outrage → regulatory tightening.

Loosening Phases

Loosening phases are also politically driven.

| Phase | Trigger | Posture |

|---|---|---|

| Reagan era (1981–) | 1970s stagflation, regulatory fatigue | SEC budget cuts, scaled-back enforcement |

| JOBS Act (2012) | Post-2008 growth slowdown | Crowdfunding, easier IPOs |

| Trump 1.0 (2017–) | Market-autonomy posture | Reg A+ expansion, lighter registration |

| Atkins / Project Crypto (2025–) | Innovation / competitiveness posture | Release 33-11412, Innovation Exemption |

Loosening phases typically follow either (i) a reaction against the costs of the prior tightening, or (ii) a politically favorable environment for markets.

What the Pattern Means

This pendulum is not accidental — it is structural.

Major market event → political outrage → tightening → market contraction → industry lobbying → loosening → market overheating → new event → tightening again.

Each cycle runs roughly 10–20 years.

So where are we now? The Gensler tightening phase (2021–2025) has ended, and Atkins's loosening phase has just begun. The pendulum has swung toward looseness.

That is why Release 33-11412 arrived. Not because the law changed. Because the political pendulum moved.

3. Crypto — Same Statute, Opposite Interpretation

The pendulum is not abstract theory. What happened in crypto regulation over the past five years proves it.

Gensler vs Atkins

The statutes have not changed. The Securities Act of 1933, the Securities Exchange Act of 1934, the Howey test (1946) — all remain on the books, unchanged. But the SEC's interpretation of those statutes has completely reversed.

| Gensler (2021–2025) | Atkins (2025–) | |

|---|---|---|

| Default position | "Most crypto is a security" | "Most crypto is not a security" |

| Enforcement mode | Regulation by enforcement (litigation) | Framework-first (interpretive rule) |

| Clarity provision | Howey applied case-by-case | Five-category taxonomy (Release 33-11412) |

| Coinbase / Kraken litigation | Actively pursued | Voluntarily dismissed (February 2025) |

| SAB 121 (custodial accounting) | Enacted; Biden vetoed override resolution (May 2024) | Rescinded; replaced with SAB 122 (Jan 23, 2025) |

What the table shows is simple: same law, same facts, opposite conclusions. The variable is who runs the SEC.

The Fate of the Sixteen Tokens

The most dramatic example is the fate of the tokens themselves.

In June 2023, the Gensler-era SEC sued Binance and Coinbase, explicitly arguing that SOL, ADA, MATIC, FIL, and roughly a dozen other tokens were "investment contract securities." The defendants stood accused of running unregistered exchanges trading these securities.

In February 2025, the Atkins-era SEC voluntarily dismissed the Coinbase suit. In March 2026, Release 33-11412 classified the same tokens — sixteen of them, including SOL, ADA, MATIC, FIL — as Digital Commodities. Not securities.

Same tokens. Eighteen months apart. Opposite classification. Did the economic substance of these tokens change in between? No. The politics did.

Congress — The Slow Clock

A noteworthy point is that Congress, on a bipartisan basis, agrees that "we need rules." The disagreement is over how strong those rules should be.

- FIT21 Act (May 2024) — passed the House 279–136, with 71 Democrats joining.

- CLARITY Act (2025) — passed the House 294–134, with even broader bipartisan support.

If the executive branch is the fast clock of the pendulum, Congress is the slow clock. But it points in the same direction. Congressional legislative effort is, in part, an attempt to dampen the pendulum's amplitude — to stop the entire regulatory framework from hinging on the views of one SEC chair.

4. Release 33-11412 Is a Beginning, Not an End

The person who acknowledged this most clearly is, perhaps surprisingly, Chairman Atkins himself.

The timeline is this: on January 29, 2026, Atkins and CFTC Chair Michael Selig jointly announced Project Crypto — an inter-agency coordination initiative for digital asset regulation. In March, the SEC and CFTC formalized that coordination through a Memorandum of Understanding. And on March 17, 2026, the SEC issued Release 33-11412, which took effect six days later.

At the time of the Release's issuance, Atkins described it as "a beginning, not the end."

That phrase carries two meanings.

A Beginning — Formal Rulemaking Is Underway

The Release is an interpretive rule. Under the Administrative Procedure Act (APA), interpretive rules are exempt from notice-and-comment requirements. They take effect quickly, but they carry less binding depth than formal rules.

The next step is Regulation Crypto Assets — a formal rulemaking, expected to be published in summer 2026, that will run more than 400 pages. What it will include:

- Innovation Exemption (Rule 750) — a 12-to-36-month sandbox allowing eligible firms to issue and trade tokens without full SEC registration.

- Capital-raising safe harbor — up to $75 million per year in exempt offerings, an expansion of the Reg A+ framework.

- Trading, custody, and clearing infrastructure — registration procedures and obligations for digital-securities exchanges, custodians, and clearing agencies.

- DTC tokenization pilot — under a no-action letter issued December 11, 2025, the Depository Trust Company will launch a three-year tokenization pilot in the second half of 2026.

- SEC–CFTC MOU (March 2026) — formalized coordination on overlapping jurisdictional questions.

Once these formal rules are in place, the Release's five-category taxonomy will operate as a working legal system.

But this is not the end. It is the starting point that the next political phase will evaluate.

Not the End — The Next Pendulum

The logic of the pendulum is simple. Loosening phases naturally lead to market activity → overheating → incident → tightening.

What could trigger the next tightening phase? Plausible scenarios:

- A major crypto failure. A token operating under the Innovation Exemption sandbox produces a fraud or systemic failure on the order of $10 billion. Just as FTX (2022) justified Gensler's tightening, a future incident could undermine Atkins's loosening.

- A DeFi incident. An incident emerges in areas that the five-category framework does not explicitly address — autonomous DeFi protocols, algorithmic stablecoins, anonymity tooling.

- A political shift. The outcome of the 2028 US presidential election could place a tightening-oriented chair back at the SEC.

- An international coherence crisis. Pressure from misalignment with EU MiCA, Japan's JFSA framework, or Korea's Virtual Asset User Protection Act could force a US course correction.

Whichever scenario plays out, the pendulum will move again. Release 33-11412 is not a permanent settlement. It is one phase's equilibrium point.

5. So What Should We Do?

Understanding this political character changes how we should approach regulatory risk.

Price Risk Across the Political Cycle

Every actor entering the current loosening phase — issuers using the Innovation Exemption, tokenization platforms, exchanges — must build a structure capable of surviving the next tightening phase. "Legal today" does not mean "legal forever."

Concretely:

- A blueprint for life after sandbox. The Innovation Exemption runs at most 36 months. What is the path to full registration after it ends?

- Voluntary disclosure and internal controls. Issuers that adopt these before the formal rules require them are the ones that survive the next tightening.

- Conservative legal interpretation. Do not rely on interpretations that are merely "permitted today." Build a structure that can also be defended under a tightening posture.

What Are the True Underlying Values?

In the endless oscillation of the pendulum, something does not move. The underlying values — investor protection, reduction of information asymmetry, prevention of fraud, anti-money-laundering. These are not negotiable in 1933, in 2026, or in 2040.

What moves is how these values are protected, not the values themselves.

For blockchain to survive the pendulum's game, it must demonstrate that it can realize these underlying values more effectively than the existing system — independent of which political phase we are in. The subsequent posts in this series take up that question.

Bridge to the Following Posts

- Post 4 (WHERE) — Where does the framework land when crossed with another jurisdiction — Korea’s 투자계약증권 doctrine and the cross-border asymmetries that result?

- Post 5 (SO-WHAT) — If blockchain itself becomes the disclosure medium, how does the disclosure obligation evolve?

- Post 6 (META) — If we accept that the pendulum will keep swinging, how do we design for it?

Epilogue

Ninety years have passed since Pecora's hearings ended. In those ninety years, the SEC has cycled through tightening and loosening more than a dozen times. In crypto, that cycle ran once more, in nine compressed years.

The next ninety years will be the same.

Securities regulation is permanently political. That is not a defect — it is the nature of how a democratic society regulates its markets.

Release 33-11412 brought remarkable clarity. But "remarkable" is not "permanent." Predicting what the next political phase will bring — and preparing for it — is the only choice we have.

The pendulum does not stop. We simply know which way it is currently swinging.

This article is Part 3 of "The New Crypto Rulebook" series. For Part 2b — the arrival of Release 33-11412 — see The Great Pivot. Next in series: Post 4 — When Lifecycle Meets 투자계약증권 (Korea).