When Lifecycle Meets 투자계약증권 — How the SEC's New Framework Lands in Korea

Series: The New Crypto Rulebook — Decoding SEC Release 33-11412 Post role: WHERE — Where does the framework land when crossed with another jurisdiction Target: ~3,000 words Audience: Industry participants, legal & compliance counsel, and policymakers navigating cross-border tokenization between the U.S. and Korea

Prologue — The Framework Crosses Borders

Post 3 closed with a clear conclusion: securities regulation is political. But "political" does not mean "local." A shift in interpretation in one jurisdiction reshapes enforcement practice in another. Especially when the second jurisdiction modeled itself on the first.

Korea's Capital Markets Act, Article 4(6) — the definition of 투자계약증권 (the investment contract security) — is a direct descendant of the U.S. federal securities law concept of investment contract. The four Howey prongs — (i) investment of money, (ii) in a common enterprise, (iii) with an expectation of profits, (iv) derived from the efforts of others — map nearly one-to-one onto the Korean statute. Korea's 투자계약증권 is, in short, a translated Howey.

That fact carries a simple consequence. If the SEC changes how it reads Howey, Korean enforcement practice will follow. It is hard to find a rational reason why it would not.

This article analyzes how Release 33-11412 lands in Korea, in four steps. (1) How similar — and how different — is the Korean statute from the U.S. statute at the textual level (§1)? (2) Which of Release 33-11412's four core interpretive changes create direct pressure on Korean practice (§2)? (3) Where does the homology break — and what about doctrinally novel concepts like lifecycle that have no Korean counterpart (§3)? (4) And how do the April-to-May 2026 developments — the Innovation Exemption, the DTC pilot timeline, Korea's STO regime going live — turn into concrete cross-border scenarios (§4)? A final section briefly addresses the non-doctrinal axes — market, politics, and public opinion — that determine how this all actually plays out (§5).

1. The Textual Comparison — Four Subtle Differences Between Howey and §4⑥

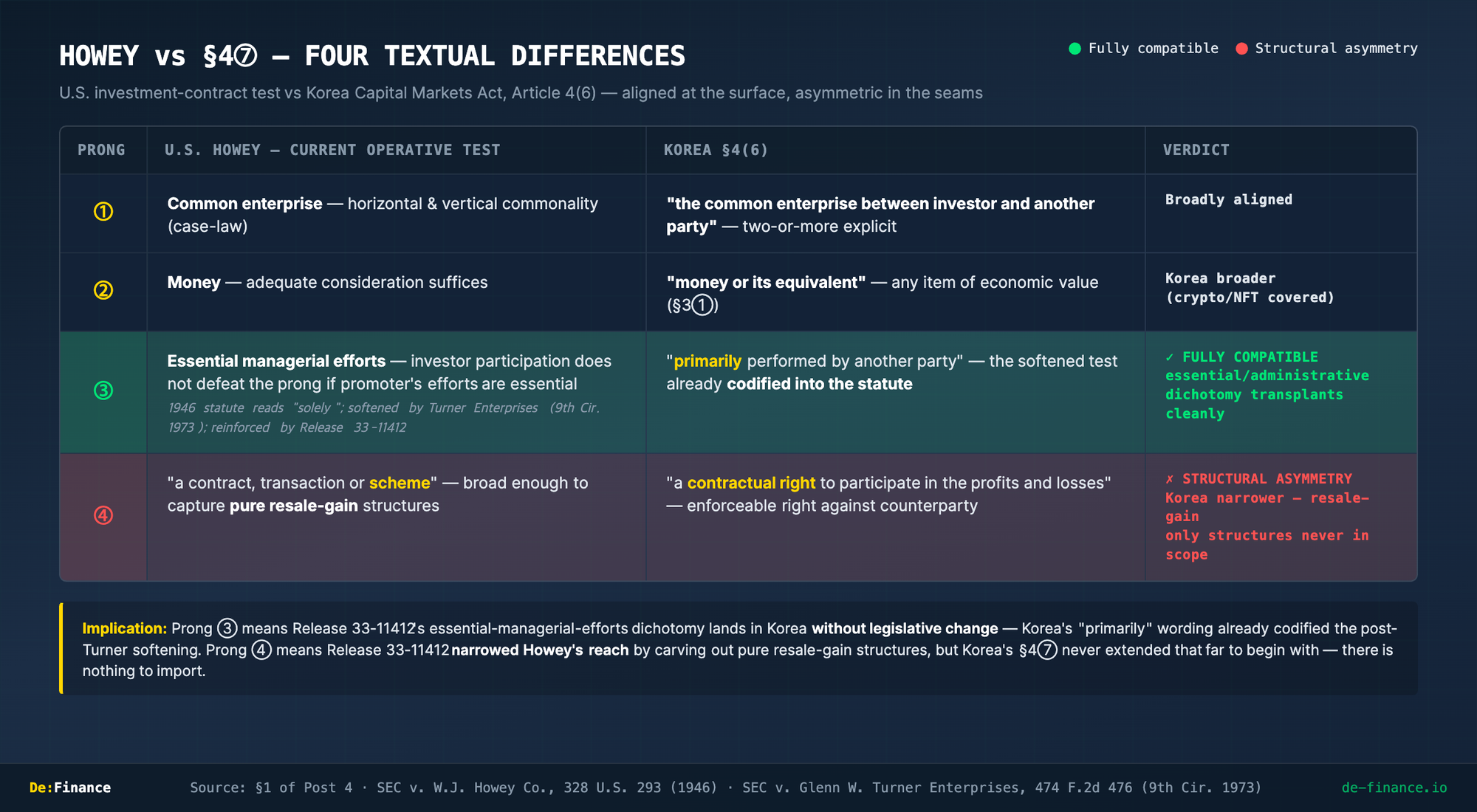

Korea's §4⑥ codified the four Howey prongs almost verbatim. But the statute introduces four structural differences at the textual level. These differences determine which parts of the SEC's reinterpretation transplant cleanly to Korea, and which parts do not.

| Prong | U.S. Federal Securities Law (Howey, 1946) | Korea, Capital Markets Act §4⑥ | Key Difference |

|---|---|---|---|

| ① Common enterprise | "common enterprise" — split by case law into horizontal and vertical commonality | "the common enterprise between that investor and another party" | Korea's text explicitly requires two-or-more participants; covers both horizontal and vertical |

| ② Investment of money | "money" — adequate consideration suffices | "money or its equivalent" (§3①) — any item of economic value | Broader in Korea. Includes non-monetary contributions like crypto assets and NFTs |

| ③ Efforts of others | "solely from the efforts of the promoter or a third party" | "primarily performed by another party" | Broader in Korea. Satisfied even when the investor partially participates |

| ④ Expectation of profits | "a contract, transaction or scheme" — broad enough to include resale-gains | "a contractual right to participate in the profits and losses of the common enterprise" | Narrower in Korea. Pure resale-gains structures are excluded |

(Source: Kim Geon-sik & Jung Sun-seop, Capital Markets Act, Chapter 2 §V.6 Investment Contract Security.)

Of these four, the most consequential are ③ and ④.

Prong ③ — "solely" vs "primarily." Howey's "solely" is the 1946 original wording, but case law softened it. Since SEC v. Glenn W. Turner Enterprises (9th Cir. 1973), the test has been read as essential managerial efforts — investor participation does not defeat the prong as long as the promoter's efforts are "those essential managerial efforts which affect the failure or success of the enterprise." Korea's statute starts from the softened position by codifying "primarily performed by another party" directly into the text.

This means Release 33-11412's essential managerial efforts vs administrative·ministerial efforts dichotomy is already textually compatible with Korean §4⑥. No legislative amendment, no novel doctrinal construction is required to absorb it.

Prong ④ — "scheme" vs "contractual right." This is where Korea is structurally different from the U.S. Howey's "a contract, transaction or scheme" is broad enough to capture resale-gains-only structures (price appreciation, secondary-market trading profits). Korean §4⑥, by contrast, requires "a contractual right to participate in the profits and losses of the common enterprise" — a right enforceable against the counterparty, not merely an expected market gain.

The consequence: structures whose only expected return is resale-gain were never within the scope of §4⑥ to begin with. Release 33-11412's new doctrine that "the crypto asset itself is not a security, only the investment contract is" is a contraction in the U.S. context, but in Korea it concerns territory that was never within the statute. There is nothing to parallel-import.

These two — the full compatibility of ③ and the structural asymmetry of ④ — are the axes that run through the rest of this analysis.

2. Four Direct Pressures Release 33-11412 Creates on Korean Practice

Release 33-11412 and the surrounding documents (2025 staff statements, the GENIUS Act) produce four interpretive changes that directly press on Korean enforcement.

2.1 Re-Reading "Efforts of Others"

What the U.S. changed. Release 33-11412 and the 2025 staff statements drew a sharp line between essential managerial efforts and administrative·ministerial efforts. PoW mining, Protocol Staking, conditional Liquid Staking, and meme-coin-adjacent activities were reclassified into the latter. Only essential managerial efforts satisfy the "efforts of others" prong.

What this means for Korea. Looking at Korean virtual-asset-exchange listing-review practice, the observable pattern is already largely aligned with this direction.

| Project element | Tendency on "efforts of others" | Pattern observed in Korean listing-review practice |

|---|---|---|

| Staking (PoS / DPoS / delegated) | ✕ Predominantly not satisfied | Largely not satisfied |

| Governance | △ Inflection point | Mixed |

| Burn / buyback | ✕ Predominantly not satisfied | Largely not satisfied |

| Rewards / dividends | △ Inflection point | Mixed |

Functional elements like staking and burn already trended toward "efforts-of-others prong not satisfied" in Korean practice. The unresolved cases cluster around governance and rewards — and Release 33-11412's essential/administrative dichotomy gives Korean reviewers a single axis ("active management vs. mechanical execution") to resolve those cases.

Operational consequence. The Korean exchange-listing practice of flagging "this token has staking / it has governance, so it might be a security" — without further analysis — is no longer defensible after Release 33-11412. Each functional element must now be shown to constitute essential managerial efforts with specific evidence.

2.2 Locking In the Non-Security Status of Stablecoins

What the U.S. changed. The April 4, 2025 SEC Stablecoin Staff Statement confirmed that Covered Stablecoins are not securities. The GENIUS Act, signed July 18, 2025, became the first federal payment-stablecoin statute and explicitly removed payment stablecoins from the securities discussion. Release 33-11412 then locked stablecoins in as an independent category in the five-fold taxonomy.

What this means for Korea. Korea's KRW-stablecoin legislative debate has not yet converged on a coherent framework as of 2025–2026 — the question of whether to address it through the second-stage Digital Asset Basic Act or a dedicated payment-stablecoin statute remains unresolved. The U.S. decision externally confirms that the Capital Markets Act track is becoming increasingly hard to defend.

Operational consequence. Classifying KRW stablecoins as securities loses international coherence. The second-stage Digital Asset Basic Act, or a dedicated payment-stablecoin statute, gains traction. If stablecoins are locked in as settlement infrastructure, Korea's tokenized-securities settlement debate (CBDC / wCBDC / stablecoin atomic-swap) is also reshaped.

2.3 The Listing-Review Frame Shifts

What the U.S. changed. Release 33-11412's five-category taxonomy offers a categorical, ex ante framework — classify by category rather than analyze token by token.

- Digital commodities

- Digital collectibles

- Digital tools

- Stablecoins

- Digital securities

What this means for Korea — homology with Korean listing-review classifications. The 12-element project taxonomy that operates in Korean virtual-asset-exchange listing-review practice is already substantially compatible with the five categories.

| Project element (12) | Release 33-11412 mapping |

|---|---|

| Staking | digital commodities (network function) |

| Lock-up / vesting | digital commodities / digital tools |

| Burn / buyback | digital commodities (tokenomics) |

| Governance | digital tools / digital commodities |

| Airdrop | digital collectibles / digital tools |

| Rewards / dividends | digital-securities suspect — turns on whether a contractual right exists |

| Fee capture | digital tools |

| ICO / token sale | digital-securities suspect — possible investment contract |

| Utility / use cases | digital tools |

| DeFi / bridge | digital commodities / digital tools |

| Promotion / marketing | digital-securities probability marker |

| Development / roadmap | digital-securities suspect |

Operational consequence. Mapping the 12-element project taxonomy onto Release 33-11412's five categories yields an immediately usable interpretive manual for listing review. A subsequent post in this series will build out that matrix.

2.4 From Enforcement-First to Rulemaking-First

What the U.S. changed. Over 2025, the SEC dismissed 12+ enforcement actions with prejudice. The regulation-by-enforcement era ended. The new policy mode runs through rulemaking and interpretive releases.

What this means for Korea. Korean securities-classification practice has run on a post-hoc-enforcement logic — FSC review → securities determination → application of the Capital Markets Act. Now that the U.S. has shifted to a taxonomy and rulemaking mode, Korea faces pressure along the same axis:

- Publish an ex-ante classification framework based on project-element criteria.

- Provide functional-category-level ex-ante classification rather than retroactive securitization of individual coins.

- Reformat FSC and DAXA checklists into publicly versioned, updatable standards.

Operational consequence. In the absence of an explicit Korean framework, Korean practice is likely to use Release 33-11412 as a reference — a natural baseline for market participants seeking global coherence.

3. Homology and the Gap — How Korea Imports the Lifecycle Concept

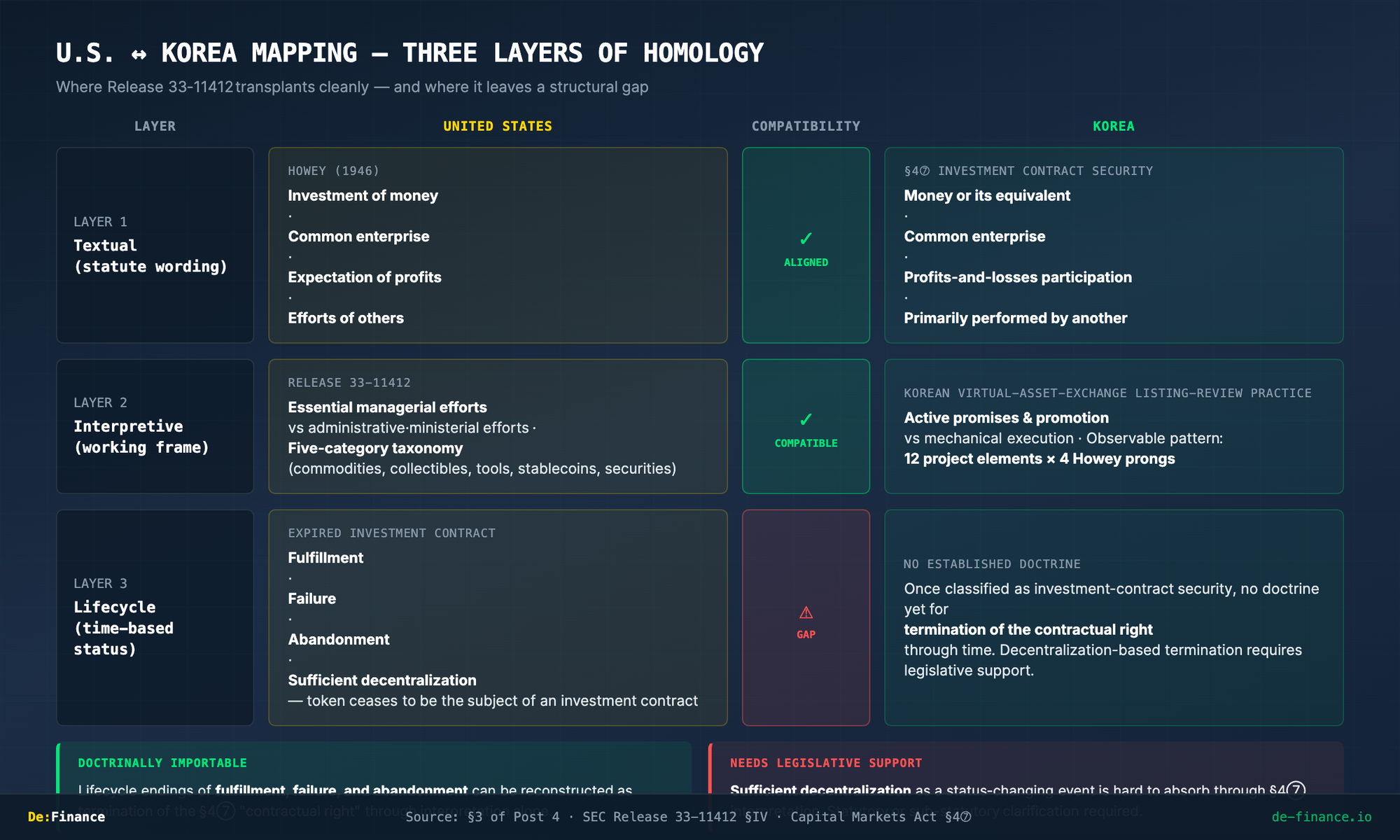

Combining §1 and §2, the U.S.–Korea mapping falls into three layers.

3.1 The Textual Layer (Already Homologous)

| U.S. Howey (1946) | Korea §4⑥ Investment Contract Security |

|---|---|

| Investment of money | money or its equivalent |

| In a common enterprise | common enterprise |

| Expectation of profits | participation in profits and losses |

| From the efforts of others | primarily performed by another party |

3.2 The Interpretive-Frame Layer (Compatible)

| U.S. Release 33-11412 | Korean virtual-asset-exchange listing-review practice |

|---|---|

| essential managerial efforts | active promises and promotion; the issuer's substantive role |

| administrative·ministerial efforts | mechanical execution; automated network functions |

| Five-category taxonomy (categorical) | 12 project elements × 4 Howey prongs |

| Lifecycle (expired investment contract) | (GAP — no established Korean practice) |

That last row is the critical one. The lifecycle concept — the doctrine that a token which once represented an investment contract may, with time, cease to do so — does not yet exist in Korean enforcement.

3.3 Importing the Lifecycle Concept Into Korea

Release 33-11412's expired investment contract doctrine has four legs. A token that was the subject of an investment contract at issuance can cease to be one when: ① the promise has been fulfilled, ② the promise has failed, ③ the issuer has abandoned the project, or ④ the network has reached sufficient decentralization. After any of these, secondary-market trading of the token is not a securities transaction.

Korean §4⑥'s "contractual right" language meets this doctrine in two directions.

Where it's compatible. §4⑥ presupposes the continuing existence of a contractual right. If the issuer has abandoned the project or fully discharged the promise, the contractual right has terminated — and from that point the token holding is arguably no longer within §4⑥. The lifecycle endings of fulfillment, failure, and abandonment can be reconstructed as "termination of the contractual right" under §4⑥. This is doctrinally importable.

Where it's not. Whether sufficient decentralization itself terminates the contractual right is unclear under Korean text. Decentralization is a change in project structure, not necessarily in the right itself. This part is hard to absorb through doctrinal interpretation alone. It requires statutory or sub-statutory clarification — either through the second-stage Digital Asset Basic Act or through enforcement guidance issued by the FSC.

Synthesis. Three of the four lifecycle endings — fulfillment, failure, abandonment — are doctrinally importable. The fourth — sufficient decentralization — is not. This asymmetry creates the most delicate grey zone in cross-border enforcement.

4. April–May 2026 Developments — Cross-Border Scenarios in Concrete Form

Two developments since Release 33-11412 took effect on March 23 directly shape Korean practice.

4.1 Innovation Exemption (Rule 750) — Atkins's April 21, 2026 Announcement

Chairman Atkins formally announced the outline of the Innovation Exemption on April 21, 2026. Eligible issuers can issue and trade tokens for 12 to 36 months without full SEC registration, subject to ① whitelisted participants, ② volume caps, and ③ periodic SEC reporting. As of May 2026, the proposal is under White House OIRA review, with formal rulemaking in progress.

Korean implication. Korea's §4⑥ has not adopted a sandbox concept. The closest analog is the FSC's Innovative Financial Services designation, but it does not exempt tokens from §4⑥ analysis. A token issued in the U.S. under the Innovation Exemption that lands in Korea must still pass §4⑥ review at the Korean exchange level. A U.S. sandbox is not a Korean sandbox.

4.2 Korea's STO Regime Goes Live in 2026 — The Race for "Token Security No. 1"

Korea's STO-enabling legislation (amendments to the Capital Markets Act and the Electronic Securities Act) passed the National Assembly, and the token-security regime goes into formal effect in 2026. The major brokerages — Mirae Asset, Korea Investment & Securities, NH Investment & Securities — have completed system buildouts through their STO Consortium, and a race for "Token Security No. 1" is expected in early 2026.

Cross-border implication. Korea's STO regime applies only when the underlying is itself a securities-grade right under the Capital Markets Act. In other words, Korea's STO regime maps precisely onto Release 33-11412's digital securities category. The other four categories (commodities, collectibles, tools, stablecoins) sit outside the STO regime and are governed by the Virtual Asset User Protection Act — and eventually by the second-stage Digital Asset Basic Act.

4.3 Three Cross-Border Scenarios

Combining the two developments above with §1–§3, the cross-border situations arising in the second half of 2026 cluster into three archetypes.

Scenario A — A token classified as a Digital Commodity in the U.S. enters the Korean market.

The flagship cases: SOL, ADA, MATIC, FIL — the 16 tokens explicitly named as Digital Commodities in Release 33-11412. They are non-securities in the U.S., but Korean exchanges are free to apply their own §4⑥ analysis. Yet because of the compatibility of prong ③ (Korea's "primarily" already encodes the essential managerial efforts test), Korean exchanges will find it hard to justify classifying these tokens as securities. De facto alignment is the rational path.

Scenario B — A token classified as non-security in Korea enters the U.S. Innovation Exemption sandbox.

A token already listed and trading on Korean exchanges enters the U.S. via the Innovation Exemption. If the SEC classifies it as a digital security within the sandbox, that classification governs only inside the U.S. jurisdiction. Korean circulation continues to follow Korea's §4⑥ analysis. A single token can legitimately hold different legal status in the two jurisdictions.

Scenario C — Non-security in both jurisdictions but governed by different regulatory regimes.

The most common case. In the U.S. the token is a digital commodity governed by the Commodity Exchange Act (CFTC jurisdiction). In Korea it is a non-security virtual asset governed by the Virtual Asset User Protection Act. The two regimes impose superficially similar duties (exchange registration, user protection, AML), but the specific obligations and enforcement tracks diverge. A multinational issuer must satisfy both.

5. The Policy Layer — A "Silent Alignment" Driven by Market, Politics, and Public Opinion

The doctrinal homology in §1–§4 is one half of the picture. The other half is enforcement intensity — which in Korea is shaped less by doctrine than by market dynamics, political signaling, and public opinion.

5.1 The Starting Observation — "Securities classification = enforcement willingness + doctrine"

In Korea, the question of whether a virtual asset is a security has functioned more like an enforcement-policy question than a doctrinal question. The statute (§4⑥) and the interpretive frame (Howey-compatible) already exist. The FSC and FSS have repeatedly directed exchanges to conduct pre-listing securities review (since July 2023). And yet:

| Domain | Guidance issued | Securities determination | Administrative action |

|---|---|---|---|

| Traditional securities markets | Ongoing | Ongoing | Ongoing |

| Token-security / fractional investment | Ongoing (post-MusicCow) | Yes (MusicCow et al.) | Yes (business restructuring orders) |

| Virtual-asset markets | Yes (2023-07 et seq.) | Effectively none | Effectively none |

In the virtual-asset domain alone, Korean authorities have moved through guidance but have not actually entered determination or enforcement. No Securities and Futures Commission decision has classified a specific virtual asset as an investment contract security. No Supreme Court ruling has spoken to it. The available trial-court rulings have actually rejected the claim (Seoul Southern District Court 2020. 3. 25, 2019가단225099, final; Uijeongbu District Court 2022. 10. 20, 2021나219018, final). This dual structure — strong guidance signals, near-zero enforcement — has long created the political conditions for a follow-the-U.S. easing path.

5.2 The Asymmetric Game — Korea Cannot Tighten If the U.S. Loosens

With the U.S. having codified the five-category taxonomy through Release 33-11412 and dismissed 12+ enforcement actions, Korea cannot credibly hold a stricter line. The costs are:

- User and liquidity outflow — Korean exchanges already operate as a KRW-walled, KYC-walled market. A stricter securities-classification regime accelerates flow to offshore CEXs and DEXs.

- Issuer attrition — global projects skip Korean listings to avoid the "only Korea treats it as a security" outcome.

- Legitimacy cost on the regulator — defending a stricter line than the SEC itself dismissed is hard to justify in public.

The rational FSC/FSS strategy is therefore follow-and-align — without an explicit easing announcement. Likely vehicles for this silent alignment: tacit migration of exchange listing-review standards toward the essential-managerial-efforts axis, staged adoption of the lifecycle concept, separation of stablecoins out of the securities track into the payments-banking frame, and absorption of Release 33-11412's five-category taxonomy as a reference into the 12-element review framework.

5.3 The Political Axis — GENIUS and CLARITY as Korean Reference Points

The U.S. GENIUS Act (stablecoins, signed July 18, 2025) and the CLARITY Act (market structure, passed by the House) function as political reference points for the Korean National Assembly. The GENIUS Act model — bank-centric, 1:1 reserves, federal supervision — is likely to be cited in the second-stage Digital Asset Basic Act debate as ground for classifying stablecoins as a payment instrument rather than a security. The CLARITY Act's digital commodity vs security dichotomy reshapes the domestic turf war between the Capital Markets Act (FSC) and the Digital Asset Basic Act (potential separate supervision).

5.4 But the Card Remains on the Table

Korean retail investors and media generally read "available in the U.S. but unavailable in Korea" as unfair discrimination. That standing public-opinion pressure makes regulatory tightening politically expensive in normal times. But when an investor-harm event hits — rug-pulls, exchange hacks, delistings — the same public opinion flips instantly to "why wasn't securities law applied?"

This intermittent spike gives the FSC and FSS the incentive to hold the securities card in reserve without playing it routinely. Silent alignment is the default. But a market incident reactivates the securities frame at any time. Neither issuers nor exchanges should treat the question as closed.

Conclusion — Implications for Korea's Second-Stage Legislation

Five lines summarize §1–§5:

- Textual compatibility is high — Korean §4⑥ is a direct descendant of Howey, and the "primarily" wording is already compatible with the essential-managerial-efforts dichotomy.

- But parallel import is partial — the "resale-gains exclusion" doctrine has nothing to import in Korea (the statute never covered it), and sufficient decentralization-based lifecycle termination needs legislative support.

- The operational frame is homologous — Korean virtual-asset-exchange listing-review practice already operates on the essential-managerial-efforts axis, and the 12 project elements map directly onto the five Release 33-11412 categories.

- Korea cannot, politically, hold a stricter line than the U.S. — the policy-arbitrage cost, liquidity outflow, and legitimacy burden all push toward follow-and-align.

- The securities card is held in reserve, not retired — market incidents reactivate the frame at any moment.

The four issues that Korea's second-stage Digital Asset Basic Act must address:

- Korean-style five-category taxonomy — rather than importing Release 33-11412's categories verbatim, publish an ex ante Korean taxonomy reconciled with §4⑥.

- Codify the lifecycle concept — anchor fulfillment / failure / abandonment in enforcement guidance or implementing decrees as §4⑥ effects. Address sufficient decentralization at the statutory level.

- Lock in the non-securities track for stablecoins — separate stablecoin regulation out of the Capital Markets Act and into a payments/banking statute, modeled on GENIUS.

- Public, versioned DAXA checklists — the infrastructure required for the transition from post-hoc enforcement to ex-ante classification.

If these four are not put in place coherently, the Korean market will use Release 33-11412 as the de facto standard while Korean authorities formally maintain a different position — a prolonged dual structure that imposes a legal-uncertainty cost on issuers, users, and exchanges alike.

Bridge to the Following Posts

- Post 5 (SO-WHAT) — If blockchain itself becomes the disclosure medium, how does the disclosure obligation evolve?

- Post 6 (META) — If we accept that the pendulum will keep swinging, how do we design for it?

This article is Part 4 of "The New Crypto Rulebook" series. For Part 3 — Securities Regulation Is Political — see De:Finance. Next in series: Post 5 — When Blockchain Becomes the Disclosure.